MENU

CLIENT ACCESS

MENU

CLIENT ACCESS

May 5, 2022

By Matthew Swerdlow and Matthew Dzbanek; Ariel Property Advisors

The Federal Open Market Committee concluded its third meeting of the year yesterday. The Fed maintained its promise to increase interest rates steadily to combat inflation and ultimately raised interest rates by 50 basis points, the highest increase since 2000. The Fed’s announcement also indicated that the Central Bank plans to start reducing its balance sheet beginning June 1. It’s expected that the Fed will continue to be aggressive via interest rate increases at upcoming meetings this year.

“There is a broad sense on the committee that additional 50 basis point increases should be on the table at the next couple of meetings,” said Federal Reserve Chair Jerome H. Powell. “We’ll make our decisions meeting by meeting as we learn from incoming data and the evolving outlook for the economy.”

The job market has started to stabilize in recent months—the nation’s unemployment rate has fallen to 3.6 percent—yet inflation has continued to skyrocket and now sits at 8.5 percent, the highest rate since December of 1981 and far above the Fed’s target goal of 2 percent. In addition to implementing aggressive open market operations, policymakers stated that the Fed will begin reducing its $9 trillion asset portfolio of Treasury and mortgage-backed securities at a rapid pace–by $47.5 billion a month for the next three months and rising to $95 billion a month thereafter. For context, the Fed’s balance sheet previously peaked at $2.25 trillion in 2008.

With a tighter monetary policy, real estate investors and borrowers should prepare for continued rate hikes and remain aware that historically, when long-term rates dip below short-term rates it has often been an indicator of a future recession. With the potential for rates to continue rising, borrowers should continue to pursue fixed-rate loans or look into purchasing interest rate caps that creates a ceiling on rate increases for the life of the loan .

“Fortunately for borrowers, the surplus of lenders in the market has created a very competitive environment to secure financing,” said Matthew Swerdlow, Senior Director, Capital Services, Ariel Property Advisors. “Our process yields multiple vetted quotes which give borrowers both clarity and closure that they’re pursuing the option with the best terms. We typically circulate any one deal among upwards of 30 lenders to ensure we’re facilitating the best execution.”

There are positives on the real estate and economic landscape that investors should be aware of and capitalize on if possible. Firstly, job growth remains strong as the aforementioned unemployment rate indicates,while vacancy rates remain low and housing demand is high, as is rent growth. With this combination of factors, real estate remains a solid hedge against inflation rates and interest rate hikes going forward.

“Investors are focusing on assets with a concentration on free market tenancy, assets with commercial rent increases that are tied to CPI, and assets with strong expense pass throughs,” said Swerdlow. “This natural hedge against inflation and strategy of minimizing exposure to rising expenses is providing borrowers confidence to continue to pursue commercial real estate as a risk-off asset at a time when the outlook in the stock market remains cloudy.”

Due to the recent surge in global commodity prices, in part influenced by the crisis in Ukraine, and continued supply chain slow-downs, there is the expectation that the Fed will move quickly to ensure that price pressures remain under control. If prices do continue to increase, and supply chain slow-downs persist, real estate prices could rise in tandem and lead to a potential decline in sales and demand as investors wait for more stabilization in the market.

When looking at the commercial real estate market, the outlook moving forward is one of cautious optimism. Those with looming loan maturities or rate adjustments should engage the capital markets as soon as possible to understand their options. Otherwise, borrowers with market rate tenancy should begin to enjoy some much needed rent appreciation that is more commensurate with their expense growth. We also expect the NYC Rent Guidelines Board to allow building owners to increase rents to rent stabilized units well above the negligent allowances of 0%-2% per year.

Multifamily Loan Programs

| Portfolio Lenders | |||

|---|---|---|---|

| Term | Interest Rates | ||

| 5 Year | 3.75% - 4.25% | ||

| 7 Year | 4.25% - 4.625% | ||

| 10 Year | 4.625% - 5.00% | ||

| Agency Lenders | |||

|---|---|---|---|

| Term | Interest Rates | ||

| 5 Year | 4.4% - 4.8% | ||

| 7 Year | 4.6% - 5.0% | ||

| 10 Year | 4.7% - 5.1% | ||

| 12 Year | 4.9% - 5.3% | ||

| 15 Year | 5.0% - 5.3% | ||

Pricing current as of May 05, 2022 and varies with LTV and DSCR

*12 and 15 year terms available as well

Commercial Loan Programs

| Term | Interest Rates |

|---|---|

| 5 Year | 4.50% - 5.00% |

| 7 Year | 4.75% - 5.25% |

| 10 Year* | 4.75% - 5.35% |

*full-term interest only available

Construction / Development / Bridge

| Type | Interest Rates |

|---|---|

| Stabilized / Core | 3.75% - 4.5% |

| Value Add / Core Plus | 4.25% - 5.75% |

| Re-Position / Opportunistic | 6.00% - 8.50% |

Pricing current as of May 05, 2022 and varies with LTV and DSCR

Index Rates

| Index | Interest Rates |

|---|---|

| 5-Year U.S. Treasury | 2.93% |

| 7-Year U.S. Treasury | 2.98% |

| 10-Year-U.S. Treasury | 2.94% |

| Prime Rate | 4.00% |

| 1- Month LIBOR | 0.85% |

| 30-Day Avg. SOFR | 0.29% |

| 1-Month Term SOFR | 0.81% |

| Ameribor Unsecured Overnight Rate | 0.44% |

| Index | Interest Rates |

|---|---|

| 5-Year SOFR Swap | 2.77% |

| 7-Year SOFR Swap | 2.75% |

| 10-Year SOFR Swap | 2.76% |

Pricing current as of May 05, 2022

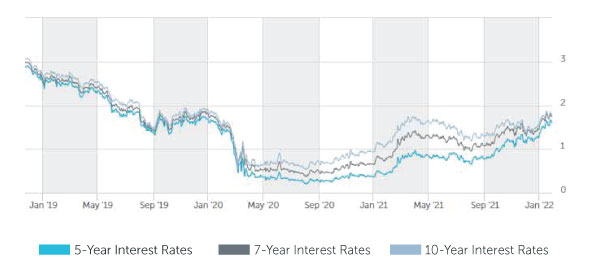

TREASURY RATES

More information is available from Matthew Swerdlow at 212.544.9500 ext.56 or e-mail mswerdlow@arielpa.com.

©2026 ARIEL PROPERTY ADVISORS