MENU

CLIENT ACCESS

MENU

CLIENT ACCESS

June 16, 2022

By Matthew Swerdlow and Matthew Dzbanek; Ariel Property Advisors

The Federal Open Market Committee concluded its fourth meeting of the year yesterday. Policymakers followed through on the expectation that they would continue to raise interest rates and approved a 3/4 percentage point increase in the primary credit rate to 1.75%. The latest rate hike is the highest since 1994 and comes in the wake of the consumer price index rising to 8.6% in May, which was higher than expected and the largest 12-month increase since December 1981. Policymakers have made it clear that additional rate increases are on the table as they seek to return the inflation rate to the Fed’s 2% objective.

“We anticipate that ongoing rate increases will be appropriate; the pace of those changes will continue to depend on the incoming data and the evolving outlook for the economy,” said Fed Chairman Jerome Powell. “Clearly, today’s 75 basis point increase is an unusually large one, and I do not expect moves of this size to be common. From the perspective of today, either a 50 or 75 basis point increase seems most likely at our next meeting. We will, however, make our decisions meeting by meeting, and we will continue to communicate our thinking as clearly as we can.”

Driven by rising energy prices (up 34.6%) and groceries (up 11.9%), inflation has remained stubbornly high, prompting the Fed to adopt an aggressive monetary policy. The June announcement follows rate increases of 50 basis points in May and 25 basis points in March. Additionally, in an effort to reduce liquidity and put additional upward pressure on interest rates, the Fed will begin this month reducing its $9 trillion asset portfolio of Treasury and mortgage-backed securities at a rapid pace–by $47.5 billion a month for the next three months and rising to $95 billion a month thereafter. For context, the Fed’s balance sheet previously peaked at $2.25 trillion in 2008.

At the June meeting, the Fed raised its target range for the federal funds rate to between 1.5% and 1.75% and noted that the median projection for the federal funds rate is 3.4% at the end of this year, 3.8% at the end of next year and 3.4% in 2024.

The U.S. job market has stayed resilient with the unemployment rate at 3.6 percent and the economy continuing to grow. However, the Fed’s Beige Book survey of economic conditions nationwide noted some concerns about an economic slowdown. Labor shortages and supply chain disruptions are the greatest challenges facing businesses. In addition, consumers have pulled back on spending in the face of rising prices and high housing prices and interest rates have dampened the residential market.

“With the yield on the 10-year Treasury note doubling since the beginning of the year and mortgage rates rising, interest rate caps on adjustable-rate mortgages have become more attractive to real estate investors in recent months,” said Eli Weisblum, Senior Director of Capital Services for Ariel Property Advisors. “We were able to negotiate for our clients an interest rate capped at 1% over the initial rate when the loan resets in year 6, at no cost to the borrower. This is used as a successful hedge against potential rate hikes so the borrower knows that they are protected for 10 years should interest rates continue on an upward trend, which results in beneficial terms for both lender and borrower.”

While free market multifamily assets in markets like New York City will always be strong, Weisblum said other asset types nationwide continue to be attractive in spite of the financial and market fluctuations throughout the industry. Assets offering cap rates above 7 percent will be highly sought-after even with mortgage rates at 5.5 percent.

“In this environment of uncertainty, it’s even more important to evaluate and source all borrowing opportunities,” Weisblum said. “Business is still getting done and we’re identifying options for clients every day. We have built an extensive network of lenders with whom we have cultivated amazing relationships that allow us to provide very competitive terms to our clients.”

Medical properties such as private emergency rooms, urgent care clinics, medical office complexes and similar assets are expected to remain in high demand moving forward, Weisblum said. Capitalizing on new expectations from the public concerning healthcare and safety, medical properties will deliver value consistently for lenders and investors alike for the foreseeable future.

Finally, industrial properties will continue to see significant activity, partially due to the flexibility they offer, as they can be easily repurposed or repositioned into warehouse, storage spaces and multifamily housing. Smaller stand-alone single tenant retail sites also are expected to remain in demand by investors with 1031 exchanges.

Real estate has traditionally served as a hedge against inflation and, in spite of interest rate volatility, there will continue to be investment opportunities in select asset classes around the country.

Multifamily Loan Programs

| Portfolio Lenders | |||

|---|---|---|---|

| Term | Interest Rates | ||

| 5 Year | 4.90%-5.25% | ||

| 7 Year | 4.85%-5.25% | ||

| 10 Year | 4.75%-5.125% | ||

| Agency Lenders | |||

|---|---|---|---|

| Term | Interest Rates | ||

| 5 Year | 4.87%-5.91% | ||

| 7 Year | 4.91%-5.70% | ||

| 10 Year | 4.77%-5.54% | ||

Pricing current as of June 16, 2022 and varies with LTV and DSCR

*12 and 15 year terms available as well

Commercial Loan Programs

| Term | Interest Rates |

|---|---|

| 5 Year | 5.20%-5.50% |

| 7 Year | 5.125%-5.45% |

| 10 Year* | 5.00% -5.40% |

*full-term interest only available

**12 and 15 year terms available as well

Construction / Development / Bridge

| Type | Interest Rates |

|---|---|

| Stabilized / Core | 4.30%-5.85% |

| Value Add / Core Plus | 5.85%-7.50% |

| Re-Position / Opportunistic | 6.25%-8.25% |

| Construction / Development |

Pricing current as of June 16, 2022 and varies with LTV and DSCR

Index Rates

| Index | Interest Rates |

|---|---|

| 5-Year U.S. Treasury | 3.44% |

| 7-Year U.S. Treasury | 3.45% |

| 10-Year U.S. Treasury | 3.37% |

| Prime Rate | 4.75% |

| 1- Month LIBOR | 1.51% |

| 30-Day Avg. SOFR | 0.77% |

| 1-Month Term SOFR | 1.48% |

| Ameribor Unsecured Overnight Rate | 0.94% |

| Index | Interest Rates |

|---|---|

| 5-Year SOFR Swap | 3.19% |

| 7-Year SOFR Swap | 3.14% |

| 10-Year SOFR Swap | 3.13% |

Pricing current as of June 16, 2022

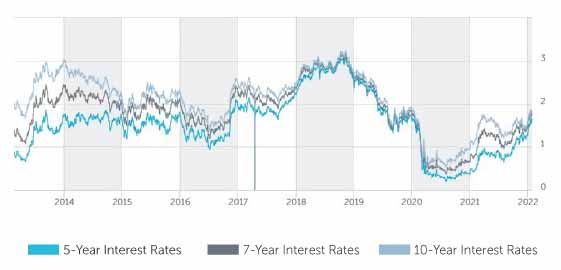

TREASURY RATES

More information is available from Matthew Swerdlow at 212.544.9500 ext.56 or e-mail mswerdlow@arielpa.com.

©2026 ARIEL PROPERTY ADVISORS