MENU

CLIENT ACCESS

MENU

CLIENT ACCESS

Originally Published in

October 2, 2023

Featuring Matthew Dzbanek, Ariel Property Advisors

Read The Article on Real Estate Capital Usa

Originally Published in Real Estate Capital Usa | October 2, 2023 | Featuring Matthew Dzbanek at Ariel Property Advisors

The US multifamily markets are largely seeing strong demand indicators, but disrupted commercial real estate capital markets are complicating the situation, writes Samantha Rowan

The US multifamily markets have been largely insulated from the storms that have engulfed other parts of the commercial real estate capital markets. But the sector is not immune to the impact of a severely dislocated commercial real estate capital market, according to panelists who participated in Real Estate Capital USA’s multifamily roundtable.

As interest rates have risen more than 500 basis points since March 2022, transaction activity has plummeted. According to MSCI, the New Yorkbased data and analytics provider, there were $55.6 billion of apartment deals through the end of Q2 2023 – a 55 percent year-on-year decline. At the same time, cap rates averaged 5.2 percent, a 70bps year-on-year change.

The reason is clear: chaos in the broader commercial real estate capital markets, according to Scott Lawlor, founder and chief executive of Miami-based multifamily developer Waypoint Residential.

But there is an important caveat that Lawlor and his fellow panelists – Aaron Krawitz, founder and chief executive of New York-based alternative lender Bravo Capital; Matthew Dzbanek, a senior director in capital services at New Yorkbased advisory Ariel Property Advisors; and Zak Klinvex, chief investment officer at Philadelphia-based development firm Post Brothers – underscored during the 90-minute discussion. “The chaos is on the capital markets side, not the fundamentals side,” Lawlor says.

This chaos has meant a steep decline in the availability of capital and a sharp increase in pricing. An August report from the Mortgage Bankers Association, a Washington, DC-based industry association, predicted a 38 percent decline in all commercial real estate lending in 2023, for an estimated total of about $504 billion. Lending in the multifamily sector is expected to decline by a similar amount, to about $299 billion, as lenders of all stripes scale back their origination programs, the MBA found.

But where there is dislocation, there is also opportunity, says Krawitz. Bravo Capital focuses on the multifamily and health care sectors, providing capital via a variety of diff erent platforms, including a bridge lending fund and a mezzanine fund offered through an affiliate. The firm is also able to provide acquisition, refinancing and construction or redevelopment financing insured by the Department of Housing and Urban Development.

(From left to right): Scott Lawlor [Founder and chief executive officer, Waypoint Residentia], Zak Klinvex [Chief investment officer, Post Brothers], Aaron Krawitz [Chief executive officer, Bravo Capital], Matthew Dzbanek [Senior director, Ariel Property Advisors]

The firm is seeing the same situation on the ground as its peers, with Krawitz citing a significant gap between buyer and seller expectations on pricing. There is also the disconnect between sponsors and lenders on proceeds, with lower loan-to-value ratios meaning there is greater demand for preferred equity and mezzanine debt.

Source: Waypoint Residentia

Bravo Capital started to see the dislocation in the capital stack play out in real time after it launched its mezzanine fund, with Krawitz noting the firm had to quickly pivot to adapt its strategy from its original focus of smaller-balance financings for acquisition or refinancing loans.

Source: Waypoint Residentia

“Before we knew it, we were doing loans as large as $20 million for individual transactions to top off deals given bank pullback. We have had some banking partners who were formerly lending at 75 percent, who are now lending at 50 percent for the same transactions,” Krawitz says.

Source: Waypoint Residentia

Sponsors seeking to line up construction loans, however, are facing somewhat different challenges.

“We are seeing that the new normal is often 65 percent leverage or so for ground-up construction nancing from the conventional bank market,” Krawitz says. “But as a HUD construction lender, we are still lending at 85 percent loan-to-case and our rates still have a 6 percent handle for non-recourse.”

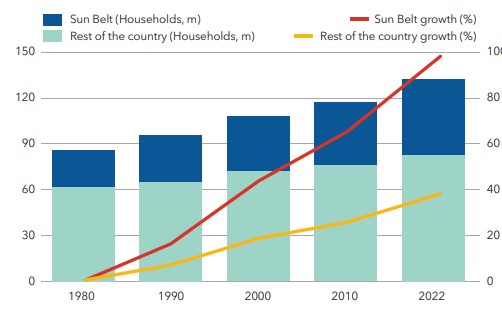

Waypoint Residential, which develops conventional apartments in and around the Sunbelt, including North Carolina, Florida and Arizona, sees the impact of the pullback in construction lending every day, Lawlor says.

“There are fewer construction lenders out there,” Lawlor says. “But even with our relationships, it is hard. Instead of getting multiple term sheets, we are getting one or two and sometimes we are even getting term sheets with syndication contingencies. There was even a situation where we had to go out and make the marriage between the lenders.“

“The chaos is on the capital markets side, not the fundamentals side” - SCOTT LAWLOR

Citing Fitch Ratings’ move to downgrade the US credit rating in August and a contemporaneous report from Moody’s Investors Service in which the agency downgraded the credit rating of several regional banks and put others on watch, Lawlor says the outlook for the near-term continues to be murky for bank participation in the construction lending market.

“The headlines from Fitch and Moody’s combined with the scare [in the regional banking market four to six months ago] makes it hard to figure out where the banks are going,” Lawlor says. “There are debt funds, of course, but there are real challenges to making those deals pencil.”

Meanwhile, Post Brothers, a class A multifamily developer which has completed or is in development on about 7,000 units, has not been in the market of late seeking financing. But it anticipates doing so in the fall, albeit with a bit of apprehension over where pricing and proceeds may end up, Klinvex says.

“Leverage points are coming in and where we used to get upwards of 80 percent construction financing, that is more like 60-65 percent on the high end and it’s also more expensive,” Klinvex says. “High rates are not great, but in situations where you’re creating an enormous amount of value, the rates won’t necessarily kill the deal.”

Although Post Brothers has not been in the market of late for a construction loan, it has been able to access the commercial mortgage-backed securities market.

“On the permanent side, one project we are coming out of a construction loan on we are taking out five-year, fixed-rate CMBS deal. That market is open, but it is not as robust as before. It is expensive, but that is just where the market is,” Klinvex says.

Dzbanek adds: “When you line up the five-year Treasury against the transaction activity, you can almost track it perfectly to the Treasury as to where activity goes. If you get a better rate, you can get closer to what the seller is asking. Once we are through this year, we can line those things up and see how they are correlated.”

A significant part of the problem facing the market today, the panel believes, is the rates are not just significantly higher and capital sources are less willing to lend. It is that intra-day and intra-week swings in rates, particularly in mid-August, are making it hard to price deals.

“In the week prior to the roundtable, the market saw a 40 basis-point movement in Treasuries,” Ariel Property’s Dzbanek says. “I quoted a loan two weeks ago and then had to call the sponsor and say, ‘We have to revise the terms that we discussed. I’ll call you in a week and let you know where the market is moving.’”

That situation is common today, as are situations in which sponsors who completed highly leveraged acquisitions in 2021 with floating-rate debt are now facing extreme headwinds as these loans near maturity.

“The floating-rate debt market is really the story here,” Krawitz says. “Sponsors who were priced to perfection when they obtained loans in 2020 or 2021, assumed rates would stay stable. But many who were too aggressive are in deep trouble right now.”

Source: Waypoint Residentia

According to Newmark’s Q2 2023 United States Capital Markets Report, the New York-based advisory is projected $1.9 trillion of loan maturities through the end of 2025. The report, published in late August, further noted that maturities in the office – and multifamily sectors – are higher than in other parts of the market. Of the $728 billion of loans slated to mature this year, about $115 billion are multifamily. There is about $88 billion of multifamily maturities set for 2024, Newmark reported.

The kicker, however, is that about a third of all maturing loans were originated at a time when valuations were at record highs and rates were at record lows.

“Leverage points are coming in and where we used to get upwards of 80 percent construction financing, that is more like 60- 65 percent on the high end and it’s also more expensive” - ZAK KLINVEX

Ariel Property Advisors, a full-service brokerage in New York that is mainly focused on the city and its five boroughs, is seeing the impact of the latter phenomenon play out in real time.

“We are doing a deal right now in New York for a sponsor who purchased a property in the $80 million range and our client is in contract in the low $30 million range. The buyer will be buying at a level that is below the debt and the lender is going to have to give some concessions to get it done,” Dzbanek says.

The firm is seeing that situation more frequently than it would like, particularly for rent-stabilized properties in northern Manhattan.

“If you gave someone a loan at 75 percent leverage and 3 percent five years ago, you’re talking about rates of 7 percent today,” Dzbanek says. “Rent stabilization is an almost uniquely New York situation, although we do sometimes see it in some of the bigger markets like Los Angeles and San Francisco.”

But situations of distress like this are largely financial and not operational, panelists say. Data from Dallas-based adviser CBRE pegged the national multifamily vacancy rate at 5 percent as of the end of June, with average monthly rents rising 2.6 percent on a year-on-year basis. This is a significant drop from the 15.2 percent rise seen in the first quarter of 2022, but a level which is more in line with the pre-pandemic five-year average of 2.7 percent, the report stated.

These numbers line up with what panelists say they are seeing on the ground.

“If you paint market rental growth with a broad brush across the Sunbelt, it is maybe 2 or 3 percent, which is not terrific, but not terrible compared to the long-term average. If you drill down, however, it is not a consistent story. Some of the markets seem to be worse, some are better, and some are in the middle. But we all knew the rent growth we saw in 2021 was not going to last forever, so this is a normalization as it relates to fundamentals,” Lawlor says.

“We are seeing that the new normal is often 65 percent leverage or so for ground-up construction financing from the conventional bank market” - AARON KRAWITZ

The bigger question to consider, Lawlor adds, is the fundamental shortage of housing in the US. While a report from CBRE is forecasting what it terms as a near-record delivery of about 716,000 new apartments in 2023 and 2024, the US continues to experience a significant shortage of units.

It is important to look at supply of multifamily units in context of population growth, Lawlor says. “If you understand the context of the problem and understand the degree to which development has failed to keep up with population growth, you will be less worried about oversupply

“I am not worried about oversupply, although there are some pockets of it. There have been decades of undersupply and as a sector, we just need to survive the capital markets. If you look at trading volume in the multifamily sector nationally, the first half 2023 was half of what it was during covid. We have a massive gap in activity.”

There is, however, a flip side to the current concerns about highly leveraged multifamily properties with floating rate debt: assets with long-term, fixed-rate debt. “When a sponsor has low fixed-rate debt on its property, it can almost be counted as an asset and the valuation spikes,” Krawitz says.

“We recently closed a 4.8 percent, fixed-rate deal at high leverage and the sponsors are now receiving unsolicited purchase offer calls at higher prices.”

With regard to pricing, the market continues to be affected by high interest rates. On the HUD front, rates are still roughly five handle, fixed-rate over the long-term while on the bridge side, rates are in the area of SOFR plus 400. For mezzanine, the conversation rates are at 12-14 percent, all-in, panelists say.

There are a few key things that enable sponsors to get a loan across the line, with panelists all echoing the most important: reliability.

“Reliability is what gets deals done today. A lot of times we hear from sponsors that they are winning deals even if they are not the highest bid because they can offer certainty of execution and a good track record,” Krawitz says.

“People want sponsors who can execute and who can handle the market cycle, just the way sponsors want lenders who are available on the closing day and don’t change your rate.”

Directly behind sponsorship is the quality of the business plan. “There is a lot of conversation around what you are doing, how you prove the model and what value do you bring,” Dzbanek says.

Getting a deal across the line also comes down to the specific asset and its location, as well as what the use will be.

“In New York, the question becomes if it is stabilized or is it free market? Is it value-add?” says Dzbanek. “In the Sun Belt, the question becomes what work has been done to the property before and how much work will be needed later? There is a strong belief that every one of my clients seems to have that rates are coming down and if they can get in on a good basis today, they’ll be in a much better place in two years.”

As lenders are working through distressed loans on their books, Klinvex says Post Brothers has been fielding some of those calls. “We have found that we are one of the first calls because of our track record. The goal is to get out with as much as they can and certainty of execution.”

Krawitz adds that a willingness to be creative is a key factor and that these solutions can run the gamut.

“The mezzanine and preferred equity solutions that we are starting to see will become more prevalent. We are also seeing structured transactions where newer sponsors who might not have the track record are bringing in JV partners with more experience.”

There is another component to this creativity and that revolves around how deals will be get done, Dzbanek says.

“We have been having conversations with lenders – not just mezzanine and preferred equity, but senior lenders as well [around the idea of formalizing relationships around origination]. It doesn’t always make sense for banks to do the sub-$10 million or sub-$20 million deals. But if they can lend the bulk of the capital to an origination platform and let them put it out with a set of guidelines, they won’t need to put it out with the same capital requirements.”

Ariel Property Advisors is starting to see a handful of debt funds follow this path. “Once this all settles down, you will see this become the next evolution, especially with the bank mergers. There are a lot fewer banks than there used to be, and they can’t keep doing the mid-market transactions anymore,” Dzbanek says.

Panelists report inbound interest from UK and Western European investors on the debt and equity side as well as Chinese, Israeli and Eastern European capital. There has also been interest from investors based in Persian Gulf countries, Japan and South American family offices.

“We have seen a lot of foreign capital enter the markets to buy Main and Main, prime assets. The thinking is that, ‘The market for this property was, say, $500 a foot and now I can buy it at $400. Even if I am going in at a perceived 5.5 or six cap, if I’m holding this for 10 or 20 years, it will trade for $500 a foot again,” Dzbanek says.

“If you gave someone a loan at 75 percent leverage and 3 percent five years ago, you’re talking about rates of 7 percent today” - MATTHEW DZBANEK

Lawlor adds that Waypoint Residential has been meeting regularly with these potential capital sources.

“On a relative basis, certain foreign investors are more receptive right now. The traditional domestic institutional players are not so much in the market right now. We found there was a little more leaning in with foreign investors. It is not to say that money is flowing easily, but it seems like there is a more reasonable conversation,” Lawlor says.

Even with the volatility in the banking sector and Fitch’s recent downgrade, investors still want to be in US real estate.

“Some of these countries have negative interest rates and other issues, and the US is still seen as a flight toward safety,” Dzbanek says. “Even after being downgraded, the US is still a better bet than the rest of the world. I would be shocked if more of this capital doesn’t start coming to the US.”

Panelists note there was more interest from South American investors than there has been during past cycles.

“We have seen groups that have been very active and have built a lot in South America and are making their first forays in the US. Historically, it was in the gateway markets – a Los Angeles or New York. That is no longer the case, there is a sense that there is a good story in secondary markets,” Krawitz says.

“We have seen a lot of interest in Texas, Florida and the Carolinas from sponsors who have not previously invested in the US.”

There is a consensus among the panelists that transaction activity is unlikely to reboot before 2024. That said, the record amount of dry powder for debt and equity that is on the sidelines will eventually be deployed. The question, however, is what will be the trigger.

“Will it be a big trade announcement? With all the dry powder, when the dam breaks, we could see a very meaningful capital flow return to the space,” Lawlor says. “At some point, we will start to see better rental growth in the Sunbelt. If we see that, along with capital beginning to flow, then the world will feel a lot better.”

While rates are not the only factor affecting the market – the direction of rates, construction costs and insurance costs, particularly in markets like Texas and Florida, are top of mind – panelists are relatively sanguine about the prospects for the longer term. The potential for a housing shortage, as well, is a key concern, as well as the long-term impact of climate change.

“The good news is that the fundamentals are good, and we can come out on the other side,” Lawlor says. “We also need to have a press conference from the Federal Reserve that is not horrible and good numbers on housing, jobs, and GDP – a few months of all of that and hopefully the world could feel very different. Getting there will be a matter of fighting through the chaos of the capital markets.”

More information is available from Matthew Dzbanek at 212.544.9500 ext.48 or e-mail mdzbanek@arielpa.com.

©2026 ARIEL PROPERTY ADVISORS